96. everything is power-law distributed

97. everything is power-law distributed

When someone writes about 137 life hacks and two of them are a) identical and b) something you have never heard of, you can’t help but dive down that rabbit hole…

So, what is a power-law distribution?

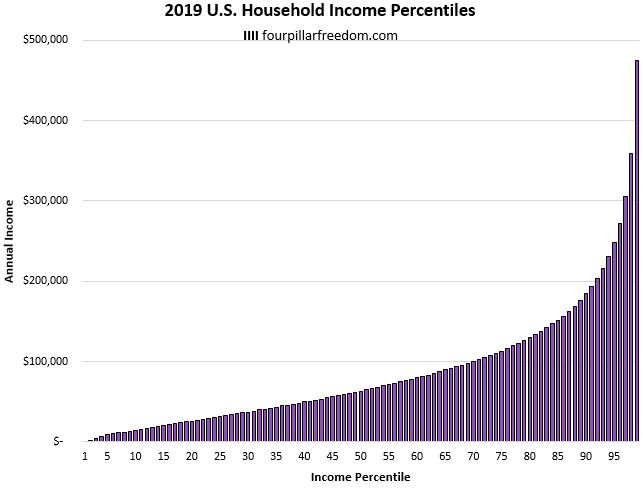

A power-law distribution is the statistical description of change that is proportional to the power of the change, in other words, change that is logarithmic, not linear. One of the classic examples of a power-law distribution curve is how income is distributed in society.

Although there are many uses for this principle in the world of finance and economics, power-law distribution can also serve as a mental model to help us understand ourselves, each other, and the world we live in.

For those who are healers, or who are studying to be healers, there are three uses of this mental model that I think are particularly relevant:

1) Hacking your studying

2) Investing in your future

3) Understanding inequities

Hacking Your Studying

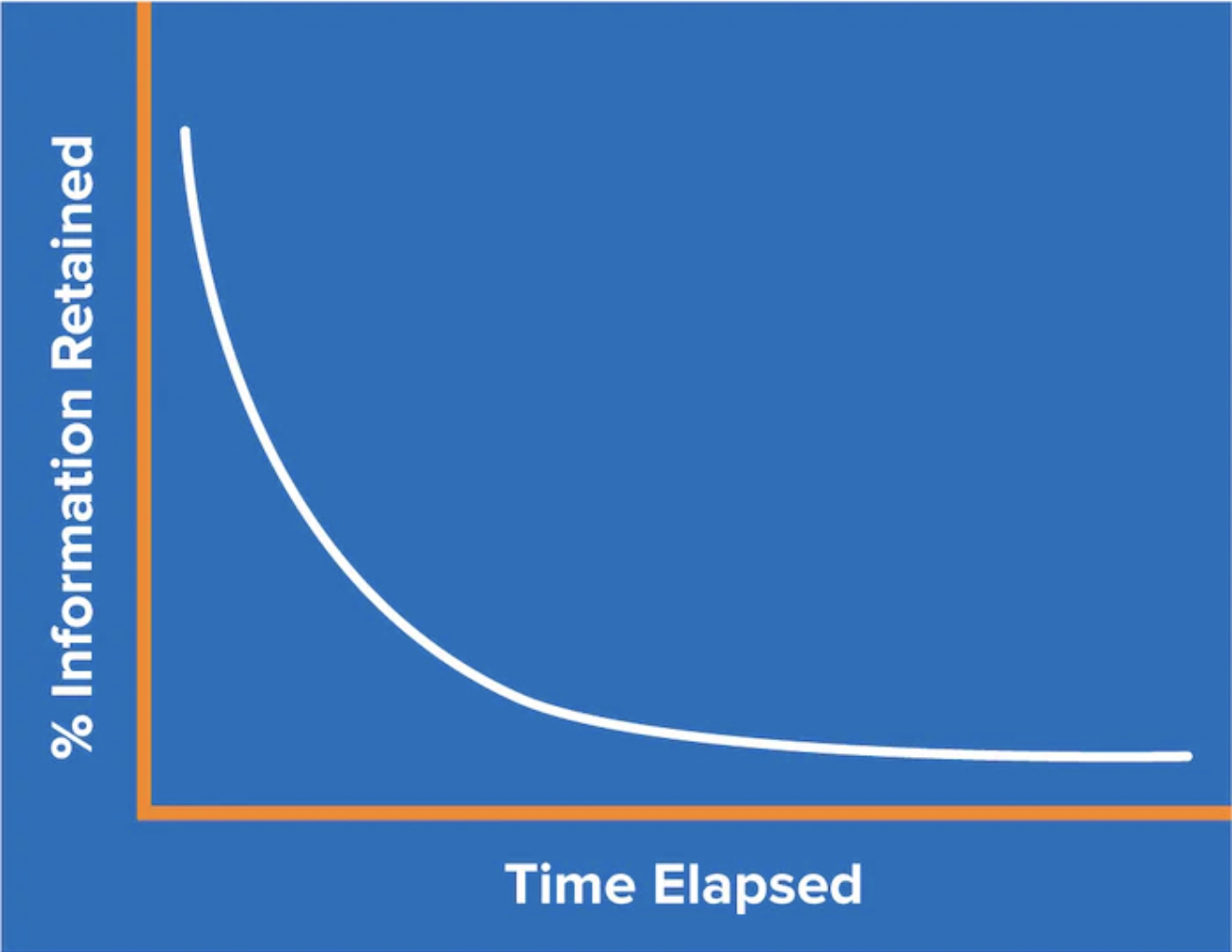

I unknowingly wrote about power-law distribution when I explained the “forgetting curve” in this post: “How to Ace the NBME Shelf Exams, In-Training Exams and Your Boards”. I recommend you read the entire post, but the take home message is this: Cramming never works if your goal is learning how to heal. What works? Repeating information you want to learn at least five times in gradually increasing intervals (ok, you type A folks… get out the spreadsheet).

The best time to plant a tree was last year. The second best time is today.

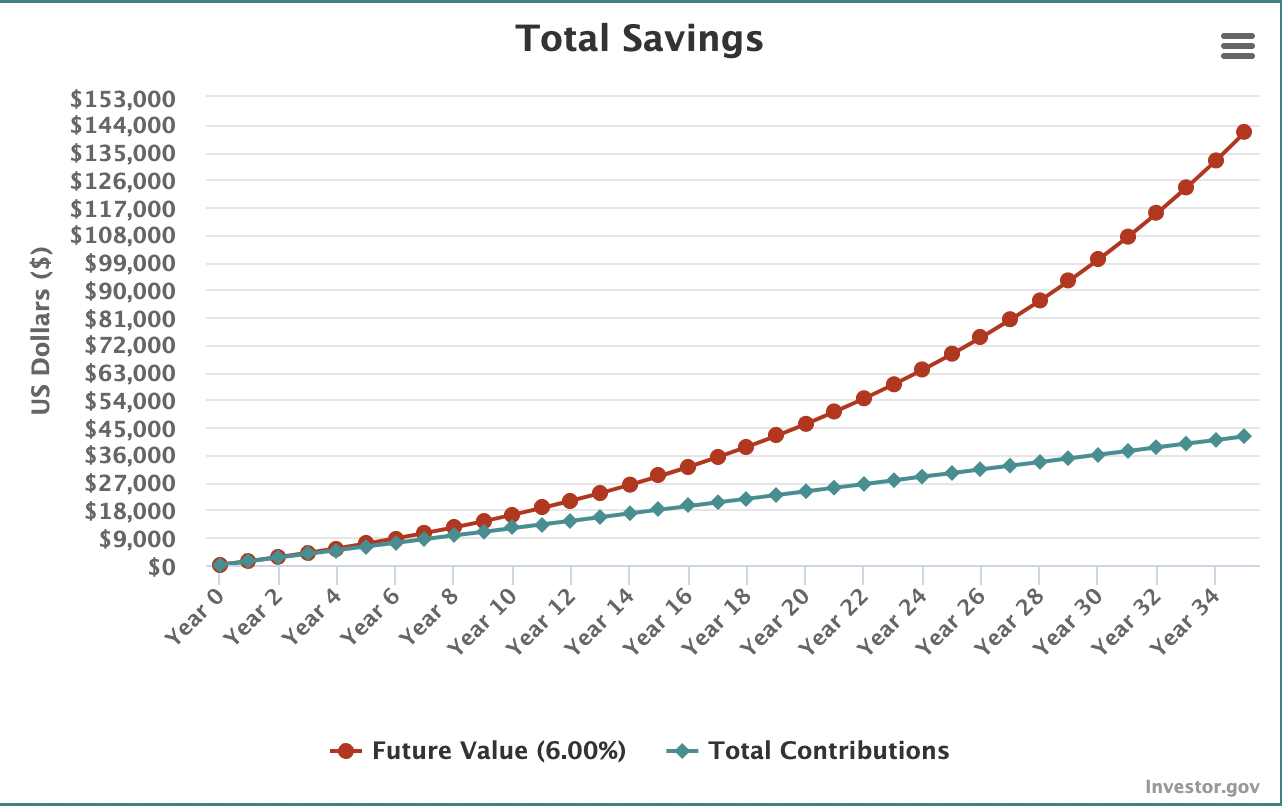

The power-law distribution also helps you understand why you need to start investing for your future – today. The chart below is what happens if you invest $100 a month starting as a new grad and keep doing it for 35 years (assuming a 6% return on your investment)

p.s. Here’s the website to do this calculation with different variables- investor.gov calculator

This kind of “investment strategy” also works for exercise. Wow, do you gain strength and fitness fast at the beginning… and how sad that it only takes about six weeks to lose most of what you previously gained if you stop (both are examples of power-law distribution). Like financial investment, investing in your body with small “doses” of consistent exercise is the best strategy. For most of us who work in a hospital, the amount of walking we do at work is close to the recommended minimum for fitness (#GoodNews). Just accumulate a few more minutes at a higher heart rate (take the stairs, speed walk to the next consult, etc), add some body weight strength exercises like pushups, and you are good!

Understanding Inequities

Investing for the future and how to hack your studying are important, but there is an even more important use for this mental model… It can help us better understanding the inequities in our society and in our work.

It’s easier to accumulate resources if you start with more. This principle is why young faculty members with limited mentorship or disproportionate service at home or at work end up not advancing. It’s why marginalized youth without resources to obtain education or connections struggle to break free from the cycle of violence and poverty. It’s why those who “have” (money, education, privilege) end up with disproportionate success (or access to care) when compared to those who started with less. Yes, there are exceptions, but they are just that… exceptions to the powerful force of power-law distribution.

There are hundreds of examples of power-law distribution including the beauty of fractals like the pattern in this beautiful head of romanesco broccoli or the curve of a beautiful seashell. (It’s worth looking at the list… some of them are fun!)

Maybe Alexey Guzey is right…

96. everything is power-law distributed

97. everything is power-law distributed

{kind=link}